Personal Finance 101: Why Financial Planning is Crucial for Young Professionals in India

Today’s generation does not have to worry about the basic necessities. These were taken care of by their parents. Their incomes are, therefore, to a large extent, disposable. Therefore, today we have a whole new investor class with a different mindset and risk appetite. We are seeing the financialization of savings. Smartphone penetration, low-cost internet, and low-cost brokerages have facilitated this. This trend is likely to continue. For India’s new generation of professionals – consultants, bankers, startup founders, and tech leaders – the first few years of earning are about lifestyle upgrades, global experiences, and the thrill of early financial independence.

But here’s the hard truth: the financial decisions you make in your 20s and 30s will determine whether you simply look wealthy now or actually build lasting wealth for the rest of your life.

Unlike previous generations of Indians, who enjoyed significant job security, the current generation is acutely aware that today’s high-flying professionals could become jobless tomorrow. Technological disruptions and geopolitical actions halfway around the world could have their echoes in your job.

The New Money Mindset

While previous generations leaned heavily on fixed deposits and gold, today’s professionals want to create and multiply wealth by making it work harder. Exposure to global markets, wealth-tech platforms, and financial communities has attracted them to equities, startups, real estate, and alternative assets. However, what’s missing is a deliberate roadmap that aligns ambition with stability. Investing without knowledge or structure leads to scattered, high-risk portfolios: half-hearted SIPs, speculative stock punts, and heavy EMIs.

Start Early

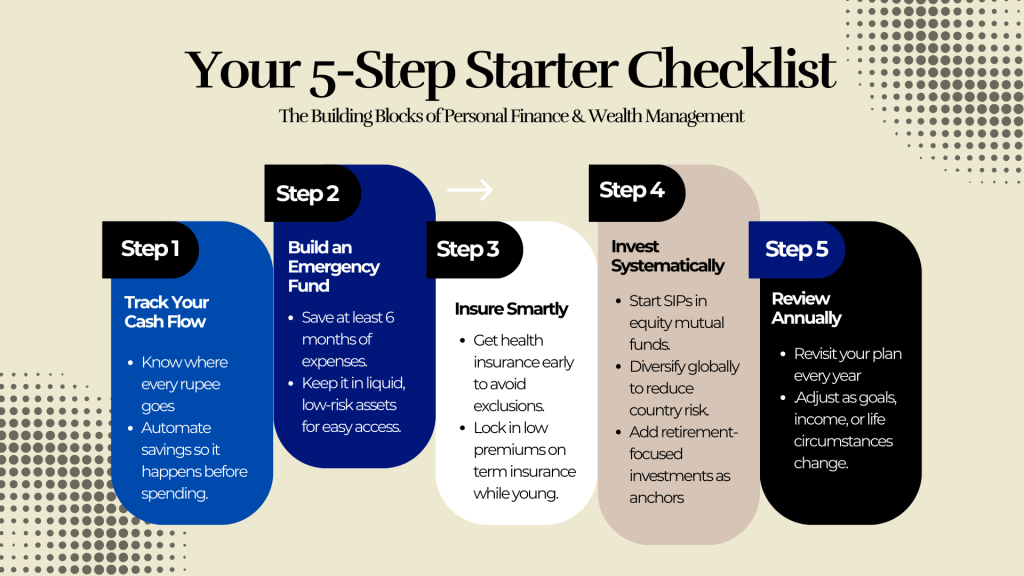

Time is the one asset young professionals truly own. By investing early, you harness compounding in ways that high salaries alone cannot replicate. A ₹25,000 SIP started at 25 can grow into multiple crores by 55. Delay the same by just a decade, and the corpus shrinks dramatically.

Early planning also allows you the flexibility to take career breaks, switch geographies, or pursue entrepreneurial ambitions without financial anxiety. More importantly, it acts as a shock absorber in case of any attrition on the employment front and consequent loss of monthly income.

Tackling Unique Risks in a Dynamic Environment

The Indian economic landscape is evolving at a breakneck pace, and with it, a new set of risks for the young professional.

- Career Volatility: Unlike a steady corporate job, a career in a high-growth startup or as a founder can come with significant income volatility. One year could be great, while the next could see a dip. A financial plan helps build a robust emergency fund and a diversified income strategy that can absorb these shocks.

- Lifestyle Inflation: As income increases, so does the temptation to spend. A new car, international vacations, and premium gadgets can eat into savings and make it impossible to build a solid financial foundation.

- Lack of Social Security: The traditional Indian family structure provided a safety net. Today’s independent and globally mobile professionals need to build their own safety net through a combination of insurance (health, life, term) and a robust retirement fund.

Building a Future-Ready Financial Strategy For YOU

For the new-age wealthy, financial planning should feel like wealth orchestration rather than restriction. What is needed is discipline, a long-term view, and persistence. Here are some tips to build a financial strategy for the long term:

- Curate your cash flow: Think of income as venture capital for your life. Track it, allocate it, and protect a consistent savings-investment share- whatever the figure is – 10%, 20%.. keep it consistent.

- Strengthen your safety net: Health insurance, Term Life Insurance, and Emergency funds are a must.

- Move beyond one-dimensional saving: Use equity funds for compounding, add global ETFs for diversification, consider REITs or alternatives for cash flow, and build retirement anchors like NPS and PPF for stability.

- Optimize taxes: Tax efficiency is wealth efficiency. Leverage 80C, 80D, NPS benefits, and capital-gains harvesting – approach taxes strategically, not reactively.

- Align money with your life goals: Your portfolio should reflect your life ambitions; whether that’s a second home, early retirement, or international exposure. Goals create purpose, and purpose drives discipline.

Technology + Advisors: The Personal CFO Model

Today’s affluent professionals blend fintech platforms with expert advice. Apps handle execution, but a professional wealth manager acts as a personal CFO, bringing clarity, strategy, and discipline to the table.

For India’s upwardly mobile professionals, the goal isn’t simply to earn more—it’s to transform income into optionality. Financial planning empowers you to take bold career moves, invest in passion projects, or retire early without compromise.

The ultimate luxury in the new India isn’t the car you drive or the brand you wear. It’s the ability to live life on your own terms, backed by a smart, future-ready financial plan.