Multi-Asset Weekly Newsletter

Global Development & Global Equities

Risk sentiment recovers as market sees faster Fed easing.

The US August CPI print was in line this week, while the US PPI surprised on the downside. The market is pricing in a cut at each of the next 3 Fed meetings this year. The market is seeing a terminal rate of around 3% getting reached somewhere around the end of 2026. The ECB kept rates on hold and suggested that it wouldn’t cut further unless there is a major weakness in the Eurozone economy.

The key event to look forward to next week will be the Fed rate decision on Wednesday. The BoE rate decision is due on Thursday, and the BoJ on Friday. It was a steady week in terms of price action. Risk assets generally had a strong week. Equities globally did well. Base Metals gained as well. Oracle shares were in the limelight this week after it reported tremendous demand for its cloud services.

Global Equities

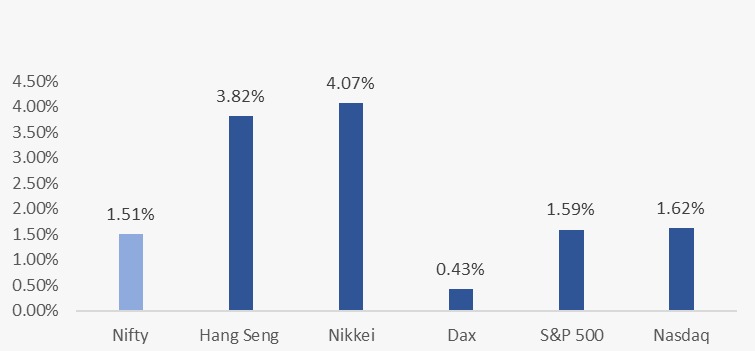

Global equities were mixed this week:

Domestic Equities

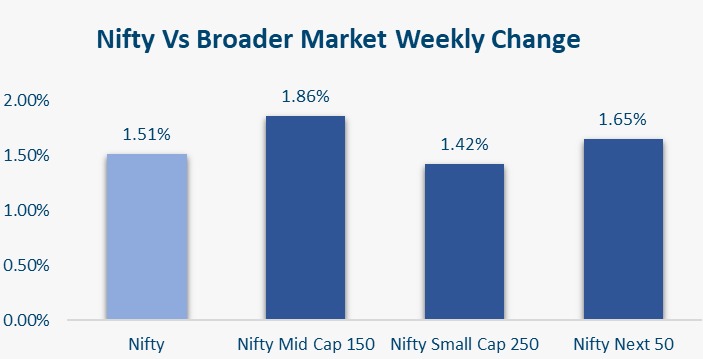

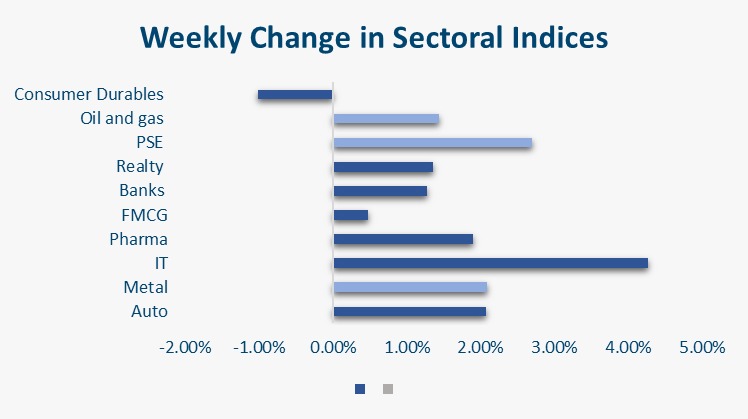

Valuations remain elevated across segments with Nifty50 trading at 22.3x trailing and 21.2x forward earnings, while midcaps (32.4x/27.8x) and smallcaps (29.2x/26.6x) continue to command a premium. On factor performance, liquidity and value led the gains, whereas growth and low volatility underperformed. Meanwhile, FPIs have turned net sellers, offloading USD 1.2 bn in the initial sessions of September. Below are the graphical representations for how key benchmark indices performed this week & how sectoral indices performed this week:

Fixed Income

Domestic August CPI print came in at 2.07%, in line with expectations

Yield on the US 2y treasury moved up 5bps to 3.56% and that on 10y ended 1bps lower at 4.06% this week. 10y Yields across the Eurozone and UK were up anywhere between 5-10bps. France 10y saw the biggest rise of 10bps as the government lost a confidence vote on the passage of budget reforms. Yield on the domestic benchmark 10y traded a 6.44-6.53% range and ended at 6.49%, 2.5bps higher than the previous week.

1y OIS is at 5.47% and 5y is at 5.69%. Overnight call rate fixings have been below the Repo rate this week. Banking system liquidity is in surplus of around Rs 2.8 lakh crores. 1y T-bill is at 5.65%, 1y CD at 6.46%

10y AAA PSU spread over Gsec is 52bps, and that of 10y AAA NBFC is around 79bps. FPIs have invested net USD 200mn in domestic debt in September so far

Private Equity & Venture Capital

Private equity and venture capital activity picked up in terms of deal count during the week ending Friday, though the overall value of investments remained nearly flat. A total of 29 companies attracted PE/VC funding compared to 24 in the previous week, with total inflows of about $363 million versus $364 million a week earlier.

The top three transactions contributed nearly two-thirds of the total funding raised, underscoring continued investor preference for larger, concentrated bets. Notably, one of these deals alone crossed the $100 million mark, highlighting selective but sizable capital deployment.

In mergers and acquisitions, activity was dominated by a single large-ticket transaction. Tega Industries, the Indian mining products manufacturer, announced the acquisition of U.S.-based Molycop for nearly $1.5 billion. Backed by Apollo Global, the deal accounted for 80% of the week’s M&A value, underscoring how strategic cross-border acquisitions continue to shape the Indian corporate landscape.

IPOs

As many as 11–12 listings are scheduled on the exchanges, making it one of the busiest weeks for IPO activity this year. Robust demand and recent SEBI clearances suggest continued momentum in the months ahead.

India’s primary markets are gearing up for a busy IPO week. Three mainboard IPOs — Urban Company, Shringar House of Mangalsutra, and Dev Accelerator — are set to open for subscription from September 10 to September 12. Together, these offers aim to raise roughly ₹2,444 crore. Key details: Urban Company’s IPO has been priced in the band of ₹98–103 per share, with a fresh issue and OFS component; Shringar House will issue shares at ₹155–165; Dev Accelerator is in the band of ₹56–61.

Alongside these mainboard offerings, the SME segment is also active. Six SME IPOs are expected to open in the same period, including names like Krupalu Metals, Nilachal Carbo Metalicks, Karbonsteel Engineering, among others. The aggregate SME issue sizes are smaller, but demand appears strong, with GMPs already reflecting investor interest.

Real Estate

SEBI has reclassified Real Estate Investment Trusts (REITs) as equity for mutual funds — a landmark regulatory move expected to expand institutional participation in real estate. By aligning REITs with equities, the change is set to boost liquidity and visibility for the asset class, positioning Indian real estate more firmly as an attractive investment avenue for both domestic and overseas investors.

Axis Real Estate, the property-focused arm of Axis Asset Management, is also looking to bring in offshore limited partners for its upcoming funds. With successful track records from earlier vehicles, including full exits with returns from its first residential fund, the firm is positioning itself to attract stronger global participation.

Commodities

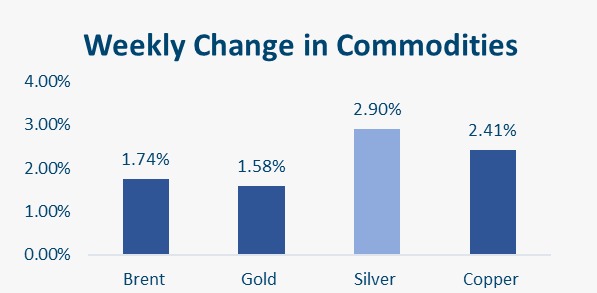

OPEC+ agreed to further increase production from October. This kept a lid on Crude prices despite Israel’s attack on Hamas officials in Qatar. Base Metals, particularly Copper, saw some positive traction this week. Precious metals continued their uptrend amid overall Dollar weakness.

Adjacent is how major global commodities moved this week:

What’s New in the World of Wealth Management?

Quant Mutual Fund’s QSIF Equity Long-Short Fund marks a pioneering development in India’s wealth management landscape as the country’s first specialized investment fund (SIF) launched under SEBI’s new framework. It introduces hedge-fund style long-short equity strategies within a regulated mutual fund structure, offering investors sophisticated market-neutral and risk-managed options previously unavailable in traditional mutual funds. This fund allows dynamic allocation between long and short positions using derivatives, aiming to deliver consistent returns across market cycles. It reflects a broader trend in India’s wealth space towards innovative, flexible, and alternative investment solutions that cater to evolving investor demands for diversification, advanced risk management, and access to complex strategies with lower entry barriers. This launch exemplifies how India’s wealth management sector is rapidly embracing global best practices and new product structures to meet the needs of high-net-worth and sophisticated investors in 2025.

Our Views: What we Like?

Equities

We continue to stick to large-cap space and select midcaps from a long-term portfolio construction point of view. Technically, Nifty50 forming a higher bottom this time at 24404 (previous 24337) is an encouraging sign. A break above 25200 could bring 25700 first, and subsequently, all-time highs back into play.

Fixed Income

We continue to remain bullish on US treasuries as faster cuts get priced in, given the deterioration in US labor market conditions and stable inflation. We had highlighted in our previous reports that 6.60% on 10y is a good level to add duration to the portfolio. We continue to believe so. We believe dips towards 5.65% on 5y OIS would he good levels to pay.

Commodities

We continue to remain bullish on precious metals given our view of overall weak Dollar. We are more bullish on Silver than on Gold. The move in base Metals this week is encouraging and we could see some positive traction there. We remain neutral on Brent.

FX

We continue to be in the camp of Dollar weakness. The Dollar’s weakness is likely to be less pronounced against EM currencies.