Billionz Multi-Asset Weekly Newsletter

Equities Face Key Resistance as IT Weakness Persists; Commodities Remain in Focus.

Global Developments:

It seems the US-Iran war has reached a stalemate. Posturing from both sides, however, is not encouraging. There seems to be little common ground to reach an agreement. The RBI rolled back measures introduced in the 1st April circular this week. It allowed corporates to cancel and rebook the same underlying exposure again and again, and allowed banks to rollover and execute transactions on a back-to-back basis with related parties. Banks can offer NDFs to clients again. The cap of USD 100mn on bank net open position in onshore derivatives, however, remains in place. The RBI, therefore, has rolled back measures that were causing operational inconvenience. Speculative curbs for banks remain in place. There is an opportunity for exporters to capitalize on higher offshore points, up to 15p in the 3m tenor.IT stocks were in focus after poor sequential revenue growth was reported in

constant currency terms for Q1 and weak guidance given by HCL and Infosys.

Global Equity Markets:

Domestic Equities

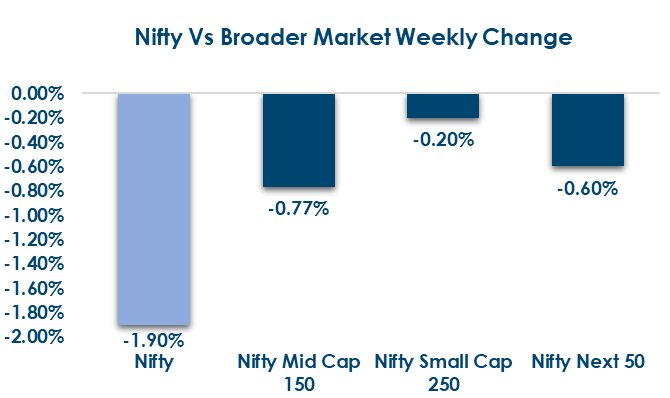

- Valuations remain elevated beyond large caps, with Nifty 50 trading at 19.9x/19.3x (TTM/forward), while Nifty Midcap 100 (33.8x/29.2x) and Nifty Smallcap 250 (30.4x/28.0x) reflect richer premiums despite some moderation on forward earnings.

- India VIX ended at 19.7 compared to the previous week’s close of 17.20.

- In terms of factors, those with high exposure to momentum outperformed while those with high exposure to growth and market cap underperformed this week.

- FII inflows surged sharply to ₹17,139 Cr this week from ₹251 Cr last week, while DII participation also strengthened to ₹9,782 Cr, indicating strong institutional buying support.

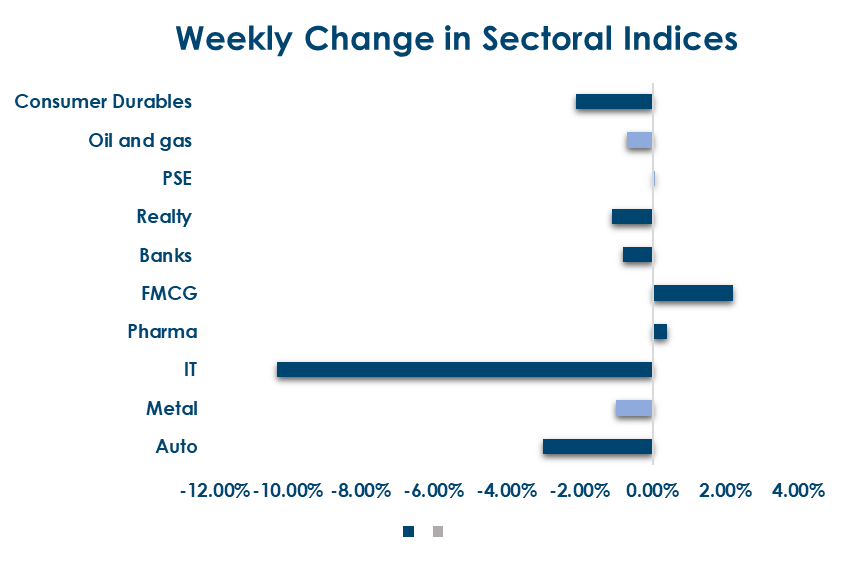

- Broad-based momentum in midcaps saw Elecon Engineering Company Ltd. (+24.2%), OneSource Specialty Pharma Ltd. (+18.2%), and Data Patterns (India) Ltd. (+16.7%) lead gains, while IT majors like HCL Technologies Ltd., Persistent Systems Ltd., and Coforge Ltd. saw notable profit booking.

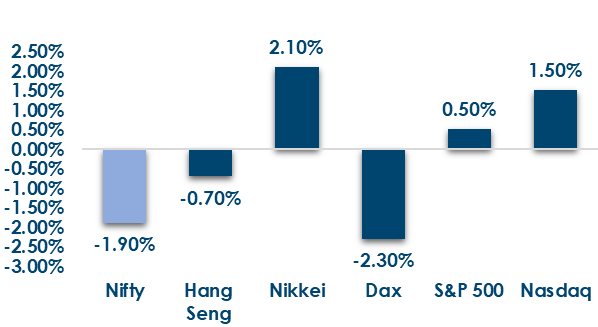

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income

- Global Rates: Global 10Y yields moved higher across major economies, led by sharp increases in the UK and South Korea (+8bps each), with China being the only outlier witnessing a marginal dip (-1bp).

- India Rates & Flows: 10Y G-Sec rose to 6.94% (+3bps) with OIS firming, while liquidity surplus eased to ~₹3 lakh crore keeping short-term rates stable.

Real Estate

- Institutional momentum in real estate is accelerating, with developers like RMZ Corp exploring $500–700M capital raises from global investors such as CPP Investments and Bain Capital to scale platforms and potentially access public markets.

- The sector is seeing rising consolidation and platform-led growth, with expansion across key cities and increasing use of JVs, REITs, and IPO routes signaling a maturing real estate cycle backed by strong institutional confidence.

IPOs

- India’s IPO market is showing early revival at the top end, with SBI Funds Management planning a ~$1.5 bn IPO, signaling renewed appetite for highquality financial services firms, driven largely bystrong domestic institutional demand.

- A major overhang may ease as the National Stock Exchange of India moves closer to listing post regulatory progress, with a ₹1,800 Cr settlement paving the way for one of India’s most significant IPOs and boosting overall market confidence.

Private Equity & Venture Capital

- Private markets saw a rise in deal activity (2 transactions) but with subdued values and no large-ticket investments, reflecting cautious investor sentiment and a shift toward smaller, early-stage bets, with selective interest in healthcare and niche manufacturing.

- M&A activity remained steady (7 deals), led by Inventurus’ $565 million Trubridge acquisition, highlighting continued strategic consolidation —particularly in healthcare—despite limited large-scale transactions overall.

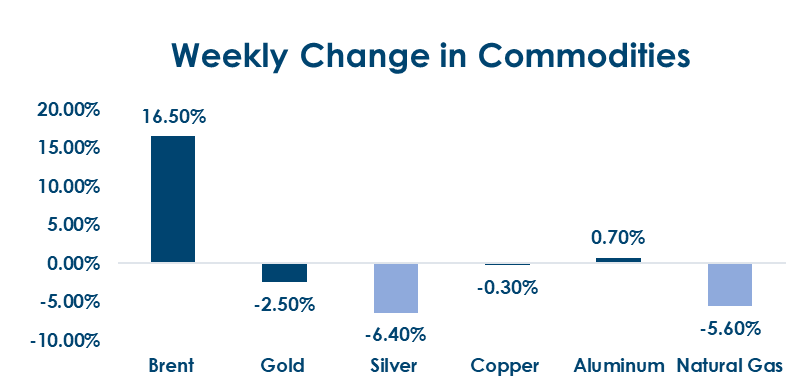

Commodities:

Energy markets led the rally this week, with Brent

and WTI surging sharply alongside gains in

European gas, while precious metals and US natural

gas declined, and base metals remained largely

range-bound.

What’s New in the World of Wealth Management?

SEBI is moving to tighten market structure with a proposal to introduce uniform dynamic price bands for all F&O stocks across exchanges, aimed at eliminating arbitrage and price distortions during expiry transitions. Currently, mismatches between NSE and BSE contract cycles create short windows where the same stock trades under different price band regimes, leading to inefficiencies in price discovery. By standardising rules—so that any stock in the derivatives segment on one exchange follows dynamic bands across all—SEBI is attempting to improve consistency, reduce volatility spikes, and enhance market integrity, especially around high-activity expiry periods.

This regulatory push comes alongside broader efforts to curb excess speculation and improve risk management in derivatives markets. Dynamic price bands, with built-in cooling mechanisms, allow for smoother price adjustments compared to fixed limits and are better suited for volatile trading environments. The move signals a shift toward more tightly regulated, institutionally aligned market structures, where reducing micro-inefficiencies and protecting orderly price discovery is becoming a priority as retail participation in derivatives remains elevated.

Our Views: What we Like?

Equities: We had mentioned last week that though we were likely to open above 24400, the key test was whether we would close the week above that. Given that we closed below 24400, that continues to be the key resistance now on a weekly closing basis. IT sector got hammered this week on disappointing sequential revenue growth reported by HCL and Infosys. The worst may not be over for the sector yet. Defensive sectors and energy did well this week, and we believe that will continue to be the playbook till external vulnerabilities remain.

Fixed Income: We expect the yield on the US 10y to be supported around 6.85% as long as crude holds above the USD 100 per barrel mark. It will be interesting to see if the government passes on the impact to consumers. If it does not, yields may continue to remain under pressure. Any level above 7% on 10y is attractive to add duration from a long-term perspective.

Commodities: We continue to remain bullish on the overall commodity complex. Any bouts of Dollar strength should be used to go long precious metals. The USD 120 per barrel mark is extremely crucial on Brent. If that breaks, we may see a vertical move this time.

FX: The dollar index is in the middle of its 96.50-100.50 range at 98.1. We expect the Dollar index to continue to remain range-bound.