Billionz Multi-Asset Weekly Newsletter

Markets Cheer Geopolitical Relief; Primary Market Sentiment Remains Cautious

Global Developments:

Israel and Lebanon agreed to a ceasefire, and Iran reciprocated that passage through the Strait of Hormuz was open to commercial vessels for the duration of the ceasefire. This news came after the onshore close yesterday. The SoH had been effectively shut down since the war began. The way talks between Iran and the US go over the weekend will be extremely crucial. The following are the key asks from both sides –

- US asks:

Nuclear Disarmament, i.e., Iran won’t pursue nuclear weapons

Permanent freedom of navigation in the Persian Gulf - Iran asks:

War reparations

Recognition of Iranian authority over the Strait of Hormuz

Immediate lifting of all economic sanctions and release of frozen Iranian

assets.

It will be a matter of what the administrations on both sides can take as wins for the people of their respective countries. At least for now, markets seem to be rejoicing in the silver lining. RBI has apparently asked oil companies to buy Dollars through a special window from SBI instead of tapping the interbank market. This is yet another measure taken by the RBI to reduce pressure on the spot USDINR.

Global Equity Markets:

Domestic Equities:

- Large caps remain relatively reasonable, with Nifty 50 trading at 20.3x (TTM) and 19.5x (forward). At the same time, broader markets stay elevated—Nifty Midcap 100 at 34.1x / 29.5x and Nifty Smallcap 250 at 30.4x / 26.5x—indicating continued premium valuations in mid and small caps despite some moderation on a forward basis.

- India VIX cooled off to 17.2 from last week’s close of 18.85

- FPIs have sold net USD 4.6bn of domestic equities in April so far

- FII inflows slowed sharply to ₹251 Cr this week (vs ₹12,543 Cr prior), while DII support moderated to ₹6,286 Cr (vs ₹13,514 Cr), indicating cooling domestic and foreign participation.

- Gallantt Ispat Ltd. (+29.6%) and Shipping Corporation of India Ltd. (+25.7%) led gains, while Jyoti CNCAutomation Ltd. (-13.7%) and Indus Towers Ltd. (-5.9%) were among the top laggards

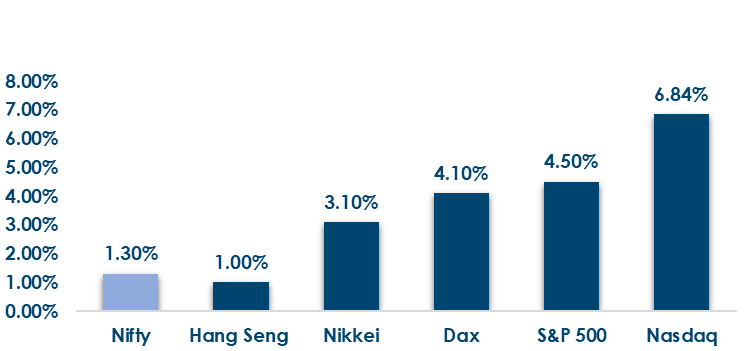

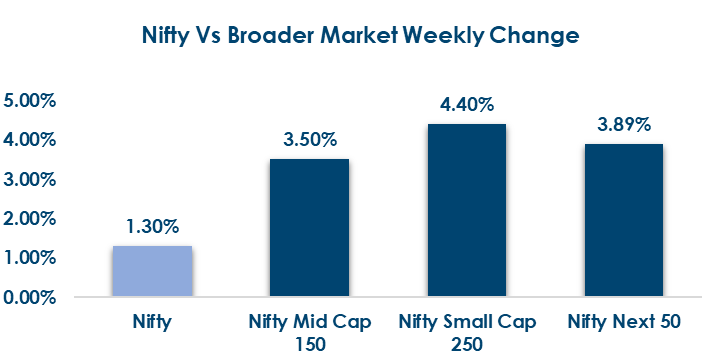

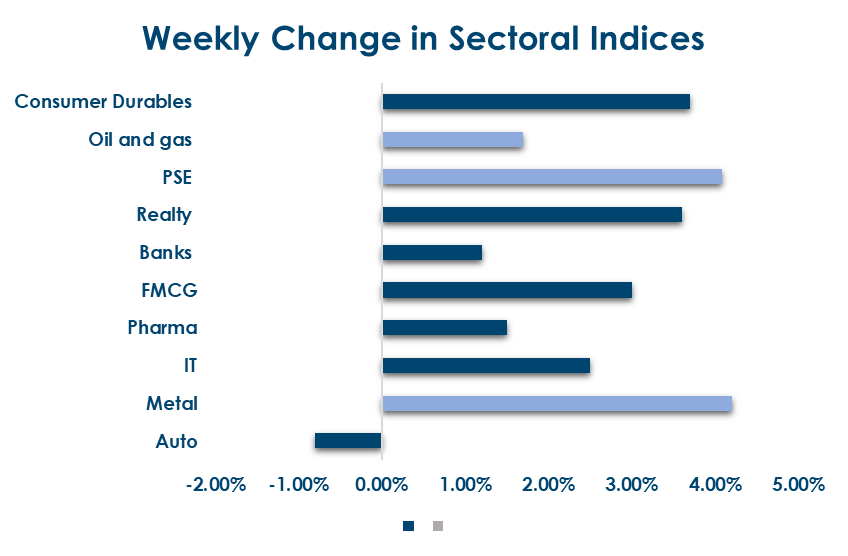

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income:

- Global Rates: Yields softened globally, led by France, Germany, UK; the US/Japan saw mild declines.

- India Rates & Flows: 10Y G-sec steady at 6.91%; OIS mixed (1Y ↓, 5Y ↑). Liquidity surplus ₹4L+ cr, spreads stable; FPIs sold USD 1.6bn.

Real Estate:

- Real estate saw strong momentum, highlighted by Mindspace REIT and 360 One Asset’s ₹3,000 crore acquisition of a 2.6 mn sq. ft. Grade A office park in Chennai, signaling sustained institutional demand for stable, income-generating commercial assets.

- The deal reflects Mindspace REIT’s expansion in key micro-markets, while transactions like Reliance Retail’s stake sale indicate ongoing sector consolidation and capital recycling by large players.

IPOs:

- Subdued IPO activity with cautious sentiment: Only one IPO—Leapfrog Engineering Services— opens this week, while GMPs remain flat, signaling muted listing expectations and a clear shift toward valuation-driven, selective investing over speculative gains.

- Listings continue, but demand remains restrained: Mehul Telecom (SME), Citius Transnet InvIT, and PropShare Celestia REIT are set to list, but flat GMP trends highlight cautious capital deployment and subdued interest, especially in SME and InvIT segments.

Private Equity & Venture Capital:

- Deal volumes fell to 19, and total funding declined ~12% to $452M, with capital heavily concentrated in a few large deals—led by Everstone’s ~$270M investment in Apothecuron— reflecting a barbell trend of marquee and small-ticket transactions, with limited mid-sized activity.

- Transactions slowed to six deals, with the key highlight being Mindspace REIT and 360 One Asset’s ~$321M acquisition of International Tech Park Chennai, while the rest of the activity remained modest and fragmented across sectors.

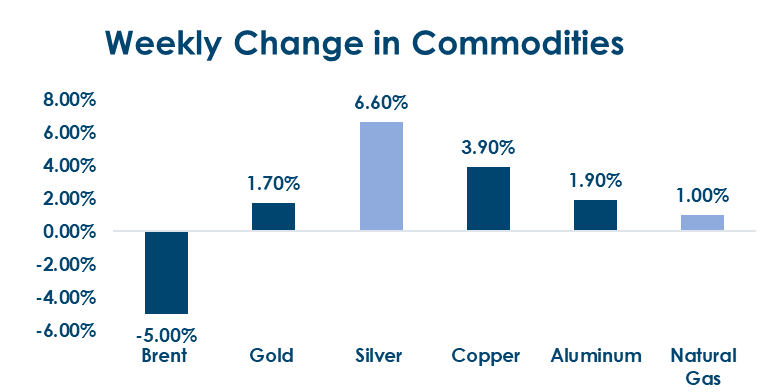

Commodities:

Crude prices corrected sharply, with WTI down 13.1%

and Brent falling 5%, while European natural gas

declined 10.8% (US gas marginally up 1%). In contrast, metals and precious metals outperformed

—copper (+3.9%) and aluminum (+1.9%) gained, while

gold (+1.7%) and silver (+6.6%) saw strong upside

momentum.

What’s New in the World of Wealth Management?

Geopolitics remained the key driver for markets this week, after US President Donald Trump signaled that the Iran conflict could be nearing an end. This triggered a sharp correction in crude prices and improved risk sentiment across Asian equities. However, markets saw some profit booking later in the week, even as foreign institutional investors (FIIs) turned net buyers after a prolonged selling phase, supported by continued domestic institutional inflows—indicating a gradual return of confidence but with caution.

On the policy front, the Reserve Bank of India took proactive steps to stabilize the rupee by managing dollar demand. It informally advised state-run oil companies to shift from spot dollar purchases to forward contracts, reducing sudden pressure on the currency. Additionally, a special credit line for oil importers was introduced to smooth dollar outflows, reflecting a more strategic approach by the RBI to manage currency volatility amid fluctuating crude prices.

Our Views: What we Like?

Equities: GIFT Nifty jumped post onshore close on news of the Strait of Hormuz being open to commercial vessels for the ceasefire duration. It will be interesting to see if the spike persists. 24400 is a crucial level on the Nifty50. We will likely open above that on Monday, but the key test will be whether we close the week above that level. A close above that level could imply that the worst is over and that we could see a V-shaped recovery. We are overweight bank and, Fin Nifty, and IT indices in our model portfolio.

Fixed Income: With the rupee cooling off as a result of the RBI’s measures, we expect rates to be kept on hold. RBI would have had to hike rates to defend the Rupee. We expect the OIS to cool off gradually. 5y OIS around 6.40% is attractive to receive with a target of 6.1%. We expect the 10-year yield to eventually come off to 6.60% once the inflation risk premium due to elevated Crude prices wanes.

Commodities: Crude prices have cooled off as the Middle East situation has de-escalated as of now. How talks proceed will be crucial, but the tolerance for higher Brent prices seems to be low from the US point of view. We have maintained that we are bullish on precious metals. Base metals also showed encouraging traction this week.

FX: Dollar index is in the middle of its 96.50-100.50 range at 98.1. We expect the Dollar index to continue to remain range-bound.