Billionz Multi-Asset Weekly Newsletter

Selective Capital Surge: Big-Ticket Deals Rise as Markets Turn Discerning.

Global Developments:

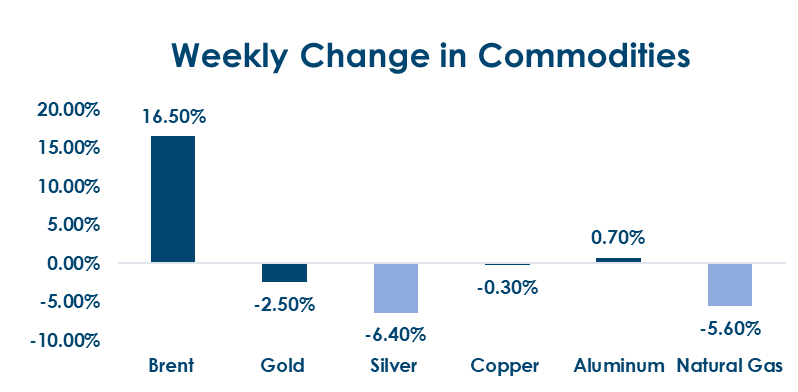

Brent shot above the USD 126 per barrel mark this week as Trump rejected Iran’s proposal to open the SoH. However it cooled off subsequently as traders stepped into a ‘wait and see’ mode, anticipating talks between US and Iran. Trump rejected the proposal sent by Iran on 1st May as well saying Iran is asking for things he cant agree to. There is a dual blockade (Iran and US side both) as of now which is choking the global oil, gas and fertilizer shipments.

Fed, ECB, BoJ and BoE all kept rates unchanged this week hut there were hawkish dissemts in Fed, BoE and BoJ. Even ECB acknowledged that short term inflation expectations had moved up. Yen was extremely volatile, having broken past the 160 mark against the Dollar on high crude prices and BoJ hold, only to stage a remarkable reversal on BoJ intervention (suspected to have sold around USD 25-30bn).

All eyes will be on the West Bengal election result on Monday. Most exit polls are suggesting a very tight race with some showing BJP ahead. The magic number for majority is 148 seats.

Domestic Equities

- Valuations across Indian equities remain elevated but moderate on a forward basis, with Nifty50 at 20x trailing and 19.5x forward P/E, while Midcap100 (33.2x/29.4x) and Smallcap250 (31.3x/27x) continue to trade at a significant premium despite some normalization ahead.

- India VIX ended at 18.46 compared to the previous week’s close of 19.7

- FPIs pulled out net USD 6.5bn from domestic equities in April. They have sold almost USD 21bn since beginning of this year.

- Considering the 24 Nifty50 companies that have reported Q4 earnings so far, the weighted average revenue surprise has been +1.2% and earnings surprise has been +3.8%.

Fixed Income:

Global Rates:

- Global 10Y yields were mixed, with South Korea (+9bps), Japan and Australia (+4bps) and the US (+3bps) higher, while UK (-1bp), Switzerland (-2bps) and China (-1bp) edged lower

India Rates & Flows:

- India 10Y ended at 7.01% after touching 7.06%, OIS rose ~12bps, liquidity stayed in surplus (~₹2 lakh cr), and spreads remained steady.

Real Estate:

- Indian real estate is becoming more institutional and focused on core cities, with developers partnering global funds and expanding REIT-led monetisation.

- Capital inflows remained steady in Q1 2026 with strong year-on-year growth despite sequential moderation, led by domestic investors (~75%+ share), while office assets continued to dominate allocations, supported by robust macro fundamentals.

IPO:

- Primary markets are operating in a two-speed environment, with strong institutional demand for large issuances like REITs driven by stable yields and improved cash flow visibility.

- SME IPO activity remains active but selective, with participation constrained by high ticket sizes, liquidity concerns, and a clear shift toward quality-focused capital allocation.

Private Equity & Venture Capital:

- PE/VC activity rebounded in value but softened in volumes, with deal count at 22 while funding surged to $420mn, reflecting a shift toward concentrated, large-ticket investments

- Key deals across jewellery, financial services, and tech (including Dholakia Lab Grown Diamond and Axis Finance) highlight selective conviction in scalable, growth-stage opportunities.

Commodities:

Brent had shot above the USD 126 per barrel mark this week as Trump rejected Iran’s proposal to open the SoH. However it cooled off subsequently as traders are in a wait and see mode, anticipating talks between US and Iran.

Our Views: What we Like?

Equities: Nifty50 seems stuck in 23600-24600 range for now. Break of 24600 could open doors for a V shaped recovery to

fresh all time highs. On the other hand break below 23600 could prolong the sideways move in Nifty50

We are overweight Fin Nifty and IT in our model portfolio.

Fixed Income: The recent selloff is seen as an opportunity to add duration, with 10Y yields above 7% considered attractive entry

levels for positioning, while at current levels receiving 5Y OIS is viewed as a strategy to convert fixed-rate liabilities

into floating exposure.

Commodities: Brent could have topped out for now and only a move again above USD 120 per barrel and weekly close above

that would entail a fresh leg of upmove in our view, we continue to be bullish on commodities overall, we believe

USD 4400–4500 is a good zone to reenter longs in Gold, USD 65–70 is a value zone in Silver, and we are bullish on

base metals.

FX: We expect G10 to remain range bound, with the broad 95.50–100.50 range on DXY continuing to hold, rupee

underperformance may reduce now as long as Brent does not cross the USD 120 per barrel mark again, and we

may see a short-term down move to 93.40, however those may be good levels to hedge imports.