Billionz Multi-Asset Weekly Newsletter

Resilient Equities Amid Consolidation; Commodities Positioned for a Dollar-Driven Rally.

Global Developments:

Axios report stating that US and Iran were closing in on an agreement to end the war turned risk sentiment around during the week. There have been incidents of attacks reported in SoH but markets continue to remain optimistic.

US labor data continued to surprise on upside with headline NFP print coming in at 115k against expected 65k.

US earnings season has been exceptionally strong. Roughly 84% of companies that have reported have delivered a positive earnings surprise for Q1.

Global Equity Markets:

Domestic Equities:

- Domestic equity valuations continue to reflect strong growth expectations, with Midcap100 and Smallcap250 commanding premium PE multiples versus Nifty50 despite some moderation on forward earnings estimates.

- Market cap weighted Sales surprise stands at 1.5% and Earnings surprise stands at 4% for Q4FY26 for Nifty50 companies (35/50 reported so far)

- FPIs have sold net USD 1.5bn of domestic equities in May so far

- India VIX ended at 16.84 compared to the previous week close of 18.46

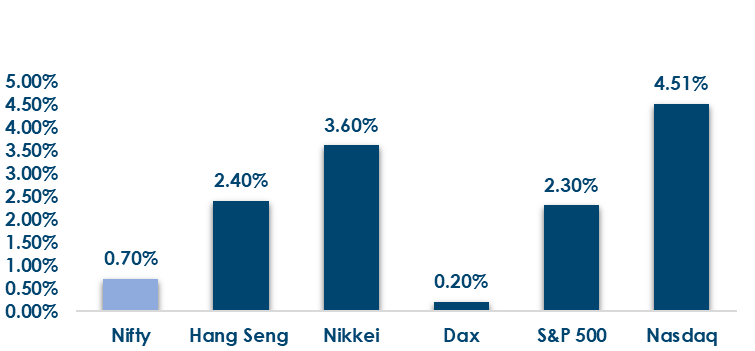

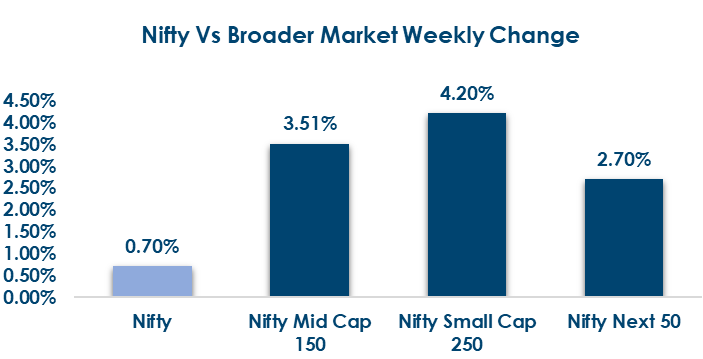

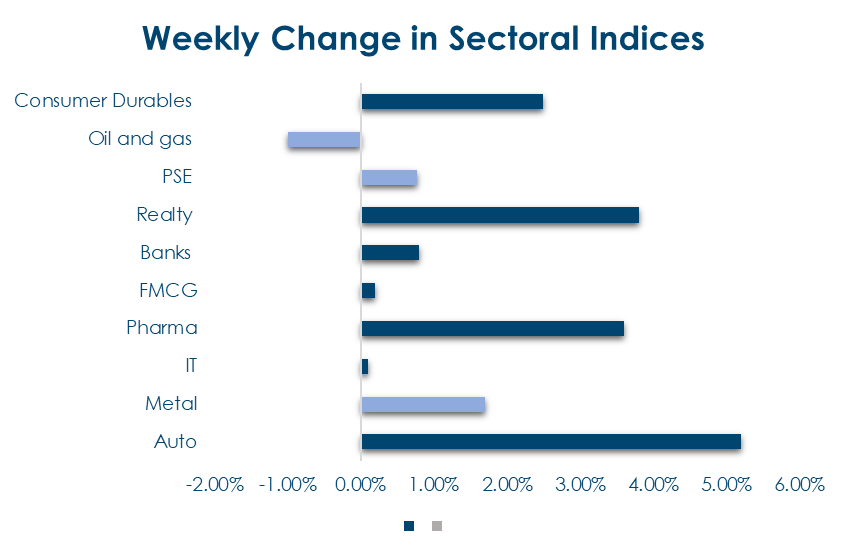

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income:

- Global bond yields softened this week, led by France (-13bps) and the US/Germany (-8bps each), as easing inflation expectations and improving risk sentiment supported demand for sovereign bonds across major economies.

India Rates & Flows:

- India’s 10-year yield closed lower at 6.98%, while surplus liquidity and softer OIS rates indicated improving domestic rate conditions.

Real Estate

- Strong institutional participation in the Bagmane Prime Office REIT anchor book reflects continued investor appetite for stable, income-generating commercial real estate assets.

- The Blackstone-backed REIT highlights the growing use of public market structures for capital recycling and monetisation in India’s maturing commercial real estate sector.

IPOs

- India’s IPO activity continues to be driven by the SME segment, with upcoming issues from RFBL Flexi Pack and Goldline Pharmaceutical reflecting steady interest in niche sectors.

- Mainboard IPO momentum remains subdued, as larger issuers stay cautious amid valuation sensitivity and evolving market conditions.

Private Equity & Venture Capital

- PE-VC activity remained steady with selective capital deployment, led by Fairfax India’s $211 million investment in IIFL Capital Services and continued interest in quality financial and consumer platforms.

- M&A activity was driven by large strategic deals, including the $1.65 billion acquisition of Rajasthan Royals, highlighting ongoing consolidation and expansion across sectors.

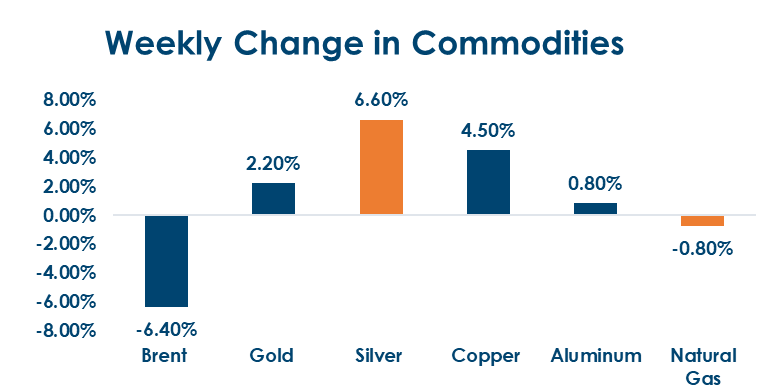

Commodities:

Brent had shot above the USD 126 per barrel mark this week as Trump rejected Iran’s proposal to open the SoH. However it cooled off subsequently as traders are in a wait and see mode, anticipating talks between US and Iran.

What’s New in the World of Wealth Management:

Electronic Gold Receipts (EGRs) are gaining traction as a key initiative to deepen commodity market participation and formalise gold ownership in India. Introduced by the Securities and Exchange Board of India, EGRs allow investors to hold and trade gold in dematerialised form on stock exchanges, improving transparency, liquidity, and price discovery while reducing dependence on physical holdings.

The framework also creates opportunities for collateralisation, structured products, and efficient gold financing by enabling seamless conversion between physical gold and electronic receipts. Although adoption remains at a nascent stage, EGRs represent a structural shift toward integrating traditional assets like gold into India’s modern financial market ecosystem.

Our Views: What we Like?

Equities: Nifty50 seems stuck in 23600-24600 range for now. Break of 24600 could open doors for a V shaped recovery to fresh all time highs. On the other hand break below 23600 could prolong the sideways move in Nifty50. We are overweight Fin Nifty and IT in our model portfolio.

Fixed Income: The recent selloff is seen as an opportunity to add duration, with 10Y yields above 7% considered attractive entry levels for positioning, while at current levels receiving 5Y OIS is viewed as a strategy to convert fixed-rate liabilities into floating exposure.

Commodities: Brent could have topped out for now and only a move again above USD 120 per barrel and weekly close above that would entail a fresh leg of upmove in our view, we continue to be bullish on commodities overall, we believe USD 4400–4500 is a good zone to reenter longs in Gold, USD 65–70 is a value zone in Silver, and we are bullish on base metals.

FX: We expect G10 to remain range bound, with the broad 95.50–100.50 range on DXY continuing to hold, rupee underperformance may reduce now as long as Brent does not cross the USD 120 per barrel mark again, and we may see a short-term down move to 93.40, however those may be good levels to hedge imports.