Billionz Multi-Asset Weekly Newsletter

Domestic Equities Navigate Global Uncertainty

Global Developments:

Iran’s Supreme leader’s adviser said talks with US were deadlocked over USD 24bn in frozen Iranian assets. He warned of a wider war, saying Iran will give a new dimension to the war by expanding military operations beyond the SoH. A hotter than expected US jobs report triggered a sell off in US equities on Friday as tech stocks sold off with long tenor yields rising. Rate cut hopes are out of the window and market is expecting a 25bps hike by end of 2026.

While the RBI kept rates and stance unchanged in yesterday’s policy, it revised GDP forecasts lower by 30bps to 6.6% and inflation forecast higher by 50bps to 5.1% for FY27. It announced a slew of measures to incentivize inflows.

1) Expanding universe of FAR bonds (no restrictions on FPI ownership of these securities) to all new issuances of 15, 30 and 40y bonds

2) Relaxing limits on short term investment by FPIs in bonds under general route

3) Concessional FX Swap for 4 months to incentivize ECBs by PSUs

4) RBI will bear full hedging cost for hedging 3-5y FCNR deposits raised by banks till 30th Sep’26

5) Restoring time for realisation of export proceeds to 9 months from 15 months.

Global Equity Markets:

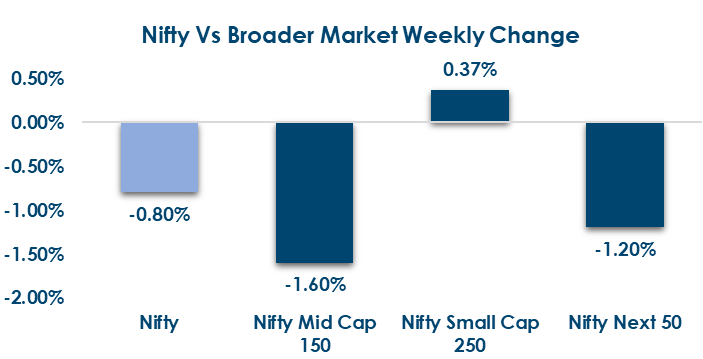

Domestic Equities

- On a trailing 12-month basis, the Nifty 50 trades at 19.8x earnings, compared with 29.3x for the Midcap 100 and 30.6x for the Smallcap 250.

- On a forward 12-month basis, valuations stand at 18.6x for the Nifty 50, 30.0x for the Midcap 100, and 23.0x for the Smallcap 250.

- FPIs have withdrawn net USD 4.5bn from domestic equities in June so far

- India VIX ended at 15.79 compared to the previous week close of 16.18.

- DII buying continued to outweigh FII selling this week, with domestic investors providing strong support to the equity market amid persistent foreign outflows.

- Aditya Infotech and Zee Entertainment were among the week’s top gainers, rising over 20%, while Jaiprakash Power Ventures and Natco Pharma led the declines.

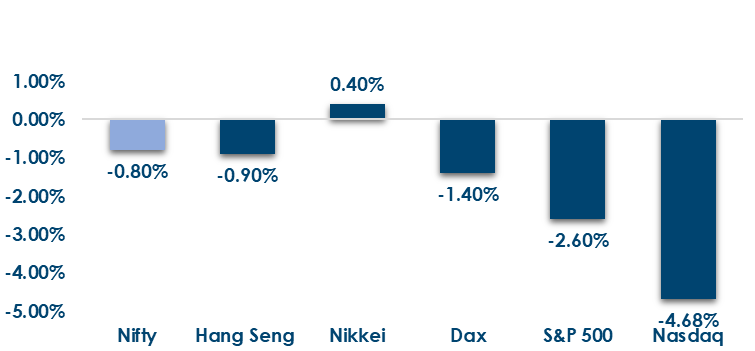

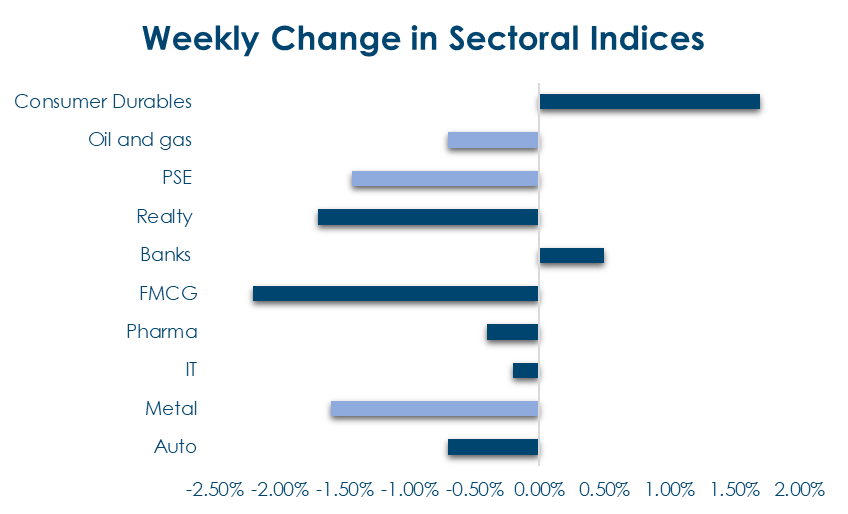

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income

Global Rates:

- U.S. Treasury yields led the global move higher this week, with the 10-year yield rising 8 bps to 4.53%, while most other major bond markets also saw modest increases

India Rates & Flows:

- India’s 10-year benchmark yield closed at 6.98%, with banking system liquidity remaining in a ₹1.8 lakh crore surplus, while FPIs have invested a net USD 600 million into domestic bonds so far in June.

Real Estate

- ICICI Prudential Alternate Investments is targeting ₹4,000–5,000 crore for its third Office Yield Optimiser Fund.

- The focus remains on fully leased, Grade-A office assets, as investors increasingly prefer stable rental cash flows and lower development risk amid improving office market fundamentals.

IPOs

- Merritronix Limited opens this week, backed by strong FY26 growth with revenue up 37% and PAT nearly doubling.

- Hexagon Nutrition returns mainboard issuance after a quiet spell, though the issue is a 100% OFS, with no fresh capital raised by the company.

Private Equity & Venture Capital

- Funding rebounded to over $263 million across 19 deals, led by a $105 million investment in Hygenco Green Energies, highlighting strong interest in clean energy and AI.

- Large transactions dominated the week, with Inox Clean Energy acquiring Vena Energy India for $627 million and Cyient buying Tao Digital for $218 million.

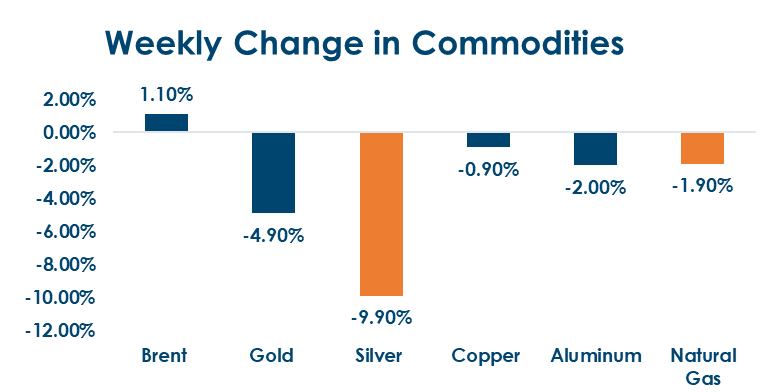

Commodities

Energy markets remained firm, with WTI crude gaining 3.6% to USD 90.5/bbl and Brent rising 1.1% to USD 93.1/bbl, while precious metals saw profit-taking, with gold down 4.7% and silver down 9.9% during the week.

What’s New in the World of Wealth Management

The RBI MPC on June 5 held the repo rate unchanged at 5.25%, the third consecutive pause following

125 basis points of cumulative cuts in 2025, as Governor Malhotra cited elevated crude near $97/bbl, the

rupee near all-time lows, and year-to-date FPI equity outflows of ₹2.47 lakh crore as the basis for

maintaining its neutral stance. The hold was widely anticipated, but the forward guidance is what

markets will reprice: a hawkish minority among economists argues that WPI at 8.3% and cumulative

fuel price hikes of 7% in CY2026 create sufficient inflationary pressure to justify a rate hike at the

August meeting, making the easing cycle’s resumption materially less certain than priced in by rate sensitive

sectors. The government has exempted FIIs from capital gains and interest withholding tax on

Government Securities, while the RBI will absorb hedging costs on fresh 3–5 year FCNR(B) deposits to

support foreign inflows and the rupee.

Our Views: What we Like?

Equities: 23150 rising window is a very strong support for Nifty50. A break below that could cause a further from of 5%, resulting in retest of recent lows. On the upside 23850 and 24300 are key resistances. Our base case for Nifty50 to remain sideways with a slight bearish bias over the next couple of months.

Fixed Income: We expect the yield on the domestic 10y benchmark to trade a 6.85-7.15% range over the next couple of months.

Commodities: We believe current levels are attravtive to add Gold and Silver to portfolio. We prefer precious metals to base metals given that we see risk sentiment being a bit negative over the medium term.

FX: We expect the Rupee to trade a 94.40-96.20 range over the next couple of months with ‘Buy on Dips’ bias.