Billionz Multi-Asset Weekly Newsletter

Bond Market Optimism Builds as Foreign Investors Return

Global Developments:

US-Iran headlines were volatile this week. We saw escalation and strikes being traded earlier earlier in the week but towards the end of the week there were positive statements coming in from US and Iran about a potential agreement for 60 days while they negotiate terms around Iran’s nuclear program. However, US and Iran have differing accounts of what is in the framework to be signed. Nevertheless Risk sentiment was positive heading into the weekend

ECB hikes rates by 25bps this week and said it would act on a policy to policy basis.

Key event to look forward to next week would be the US Fed rate decision, Kevin Warsh’ first policy as Fed Chair. Market is expecting rates to be kept unchanged. BoE is also expected to maintain status quo while BoJ is expected to hike by 25bps.

Domestic Equities

- Nifty50 is trading at 19.8x trailing and 18.9x forward earnings, reflecting relatively reasonable large-cap valuations.

- Midcaps and smallcaps continue to command richer valuations, with the Midcap100 trading near 30x forward earnings.

- FPIs have withdrawn net USD 6.6bn from domestic equities in June so far.

- India VIX ended at 14.72 compared to the previous week close of 15.79.

- Aegis Logistics (+22.6%), CarTrade Tech (+19.8%) and Caplin Point Laboratories (+18.4%) were the top gainers this week.

- Oil India (-13.6%), OneSource Specialty Pharma (-9.9%) and Wipro (-9.2%) were among the biggest laggards.

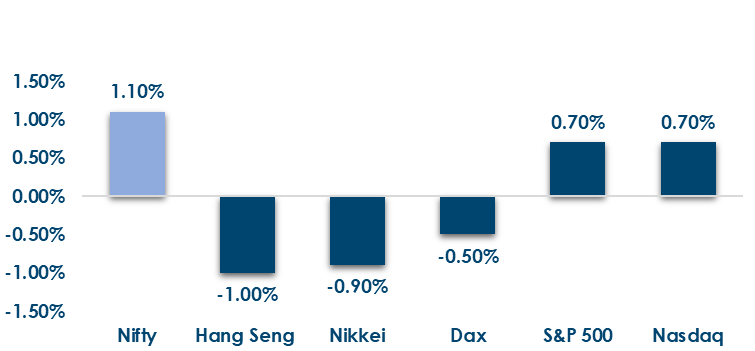

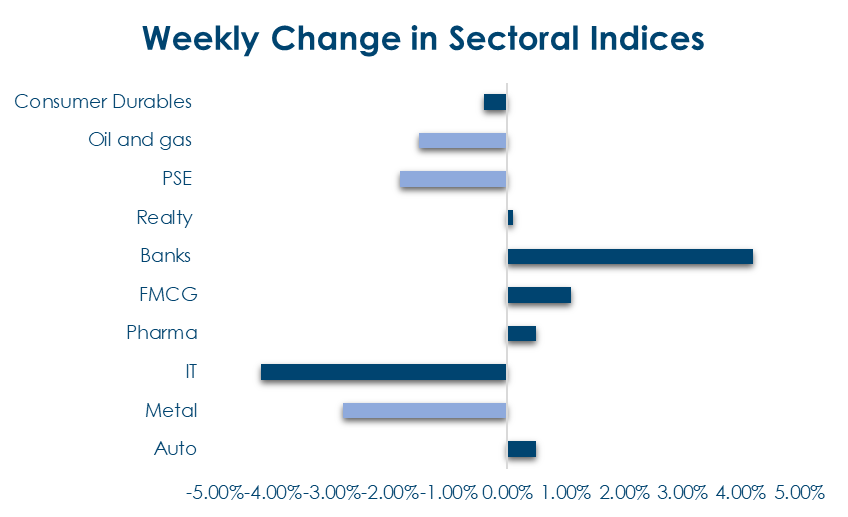

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income

Global Rates:

- Bond yields declined across major economies this week, led by Korea (-18bps) and the UK (-11bps), reflecting easing inflation concerns and growing expectations of policy support.

India Rates & Flows:

- India’s 10-year benchmark yield fell 10bps to 6.89%, supported by surplus liquidity, lower OIS rates and continued FPI inflows of USD 2 billion into domestic bonds in June.

Real Estate

- ICICI Prudential Alternate Investments is planning to launch its third office-focused real estate fund with a target corpus of ₹4,000–5,000 crore, highlighting continued investor appetite for income-generating commercial assets.

- Demand remains concentrated in premium, fully leased office properties, with recent acquisitions by institutional investors and REITs reflecting confidence in India’s commercial real estate sector.

IPOs

- Susan Electricals’ ₹70 crore SME IPO, the largest issue this week, has attracted investor interest with a GMP implying nearly 20% upside, supported by optimism around India’s power sector capex cycle.

- Liotech Industries’ ₹36 crore SME IPO is set to open next week, while the mainboard IPO market remains quiet as larger issuers await more stable market conditions before launching offerings.

Private Equity & Venture Capital

- PE/VC activity rebounded strongly this week with 30 deals raising nearly USD 239 million, reflecting improving investor sentiment and healthy early-stage funding activity.

- Clean energy and AI remained key investment themes, with GPS Renewables and Equal AI leading fundraising activity alongside several deep-tech and innovation-driven startups.

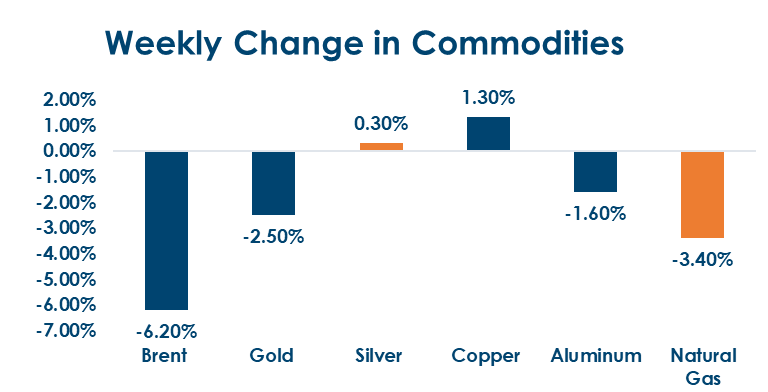

Commodities

Crude oil led declines this week with WTI and Brent falling 6.2% each amid easing supply concerns, while industrial metals remained resilient as copper gained 1.3%; precious metals were mixed with gold down 2.5% and silver marginally higher.

What’s New in the World of Wealth Management

The government’s June 5 ordinance removing taxes on foreign investments in Government Securities started showing results this week — foreign investors added ₹8,795 crore to their G-Sec holdings within days of the announcement. Standard Chartered expects $5 billion to flow in soon, and if India gets included in Bloomberg’s global bond index, an additional $25 billion could arrive over the next 10 months. That said, three operational hurdles still need to be resolved — Euroclear settlement, trading process automation, and fund registration — before India can attract the full scale of global fixed income capital. The RBI’s move to absorb hedging costs on fresh NRI FCNR deposits until September is a positive step to attract dollar inflows and support the rupee, though how much actually comes in will depend on how aggressively banks go out and mobilise these deposits.

Our Views: What we Like?

Equities:

Equities recovered on Friday on optimism around US-Iran agreement. IT sector continues to underperform. We expect the Nifty50 to trade a 23100-24300 range over the next few weeks. We believe active sector allocation and stock selection are important in a sideways market. We are overweight IT and Bank & Financial stocks in our model portfolio.

Fixed Income:

Pressure on domestic bonds eased as Brent came off. Tax relaxation and other measures are already showing impact with flows beginning to come in. Yesterday’s CPI print was lower than expected. We expect the 10y to trade a 6.80-7% range over next few weeks.

Commodities:

We believe current dip in gold and silver along with Rupee cooling off offer an attractive opportunity to increase allocation. We remain bullish on base metals as well, especially Copper.