Billionz Multi-Asset Weekly Newsletter

Markets Climb Wall of Worry as Liquidity Remains Supportive

Global Developments:

US-Iran interim peace deal was signed this week, opening up a 60 day deadline to reach a final deal. US and Iran will negotiate during this period, mainly on future of Iran’s nuclear program.

We had 3 key central bank rate decisions this week:

Fed delivered a hawkish hold this week. 9 out of 18 members see a rate hike by end of the year. Market is pricing in 1.5 hikes of 25bps by the Fed until December

BoE also kept rates unchanged. BoJ hiked 25bps to 31 year high of 1% and sounded hawkish.

Domestic Equities

- The Nifty50 trades at 20.1x trailing and 19.2x forward earnings, indicating relatively reasonable valuations compared with broader market segments.

- Midcap valuations remain elevated at above 30x earnings, while smallcaps trade at 27.5x trailing and 25.3x forward earnings, reflecting continued optimism around growth prospects.

- FPIs have withdrawn net USD 6.3bn from domestic equities in June so far

- India VIX ended at 12.97 compared to the previous week close of 14.72.

- The New India Assurance, HFCL and Schneider Electric Infrastructure emerged as the top gainers this week, advancing 32.4%, 22.0% and 20.4%, respectively

- Tata Motors Passenger Vehicles, Ola Electric Mobility and Infosys were among the top laggards, declining 7.8%, 7.6% and 5.8%, respectively.

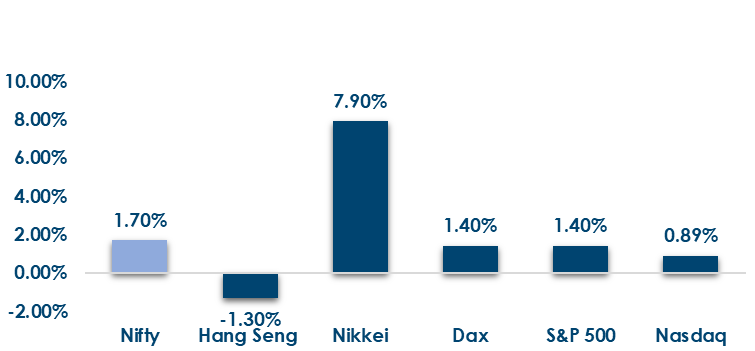

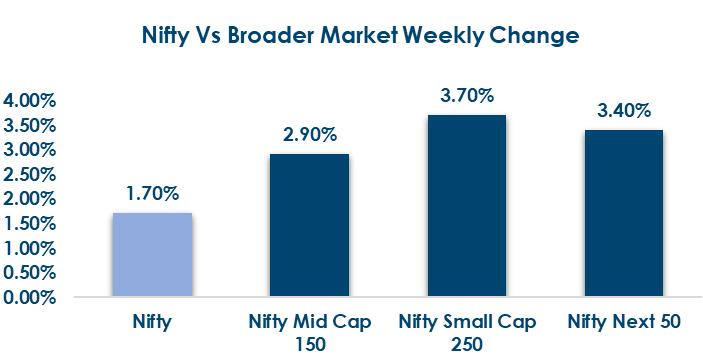

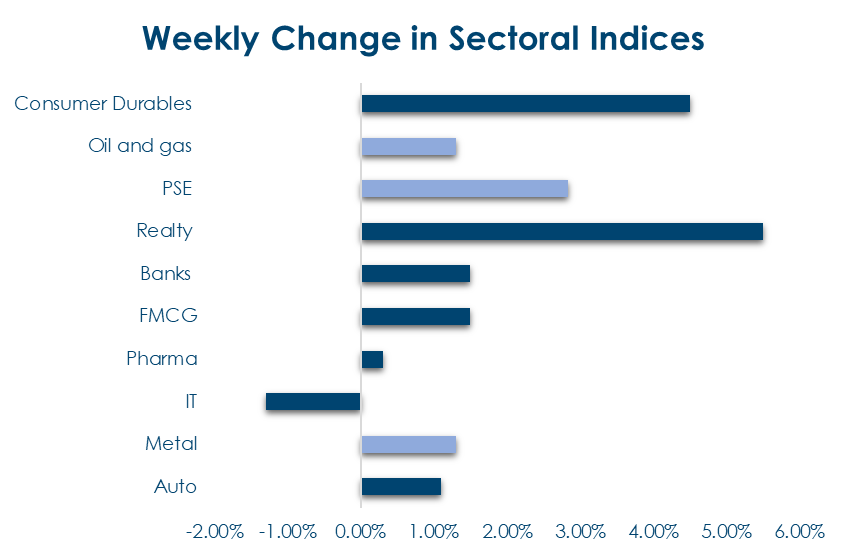

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income

Global Rates:

- Global sovereign bond yields were mixed this week, with US and Swiss 10-year yields easing by 2bps, while Japan saw the sharpest increase with a 7bp rise and European yields edged higher

India Rates & Flows:

- Domestic bond yields remained range-bound, with the 10-year benchmark ending marginally lower at 6.88%, supported by near-neutral banking liquidity and continued FPI debt inflows of USD 3.1 billion in June so far.

Real Estate

- Rising AI adoption, cloud computing demand and data localisation requirements are accelerating capacity expansion plans across India’s data centre sector.

- Strong institutional interest and increasing investments continue to strengthen the long-term growth outlook for India’s data centre infrastructure.

IPOs

- The primary market is set for its busiest week of the month, with over ₹1,800 crore of issuances spanning leisure, IT services, textiles and fintech.

- Waterways Leisure Tourism’s ₹585 crore issue offers investors a rare opportunity to participate in India’s growing premium cruise and leisure consumption story.

Private Equity & Venture Capital

- PE/VC investments crossed $1.1 billion this week, led by a $740 million investment in CtrlS Datacenters, underscoring strong investor interest in India’s data infrastructure opportunity.

- Capital continued to flow into AI and energy transition businesses, with Sarvam AI and SolarSquare attracting significant investments amid growing confidence in long-term technology and sustainability trends.

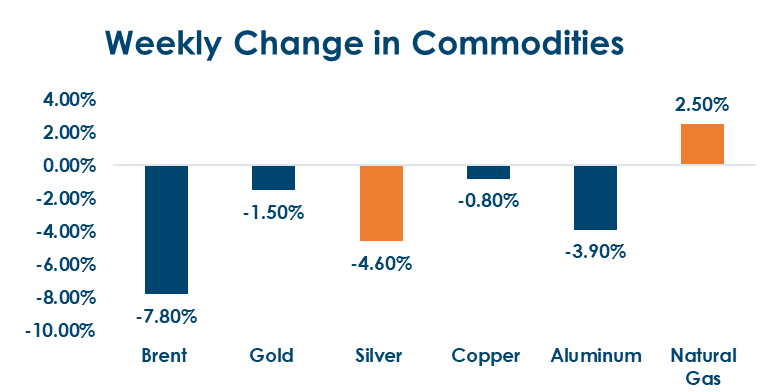

Commodities

Commodity markets witnessed a broad-based correction this week, with energy prices leading the decline as WTI crude fell 8.7% and European natural gas dropped 10%, while precious metals and industrial metals also ended the week in negative territory.

What’s New in the World of Wealth Management

This week was marked by two key developments. Reliance Industries filed the DRHP for Jio Platforms with SEBI, setting the stage for what is expected to be India’s largest-ever IPO, with valuations estimated in the $133–180 billion range and a pure fresh-issue structure aimed at funding future growth. In fixed income markets, foreign investors continued to return to Indian government bonds following recent tax relief measures, with inflows of around $2.2 billion over the past nine sessions. However, a hawkish US Fed and evolving global rate expectations are likely to keep domestic 10-year yields range-bound near 6.85–6.90% in the near term, even as the broader structural story for Indian bonds remains supportive.

Our Views: What we Like?

Equities

Strength in US equities continues overall. There are pockets of concern, especially traditional IT. Domestically too IT underperformed this week and that is keeping index gains capped. 23600 is a major support for Nifty50 and 24250 a major resistance. Break on either side could result in a 5% move in that direction. We are overweight Bank Nifty, Fin Nifty, Chemicals and REITs in our model fund.

Fixed Income

We are seeing FPIs inflows into domestic bonds and that should keep yields capped. Inclusion of India bonds in Bloomberg index could be a positive trigger. We expect the 10y to trade a 6.70-7% range over next several weeks. Raising ECB in USD and converting USD floating to INR floating seems attractive. OIS term premium is attractive to receive.

Commodities

We believe gold and silver allocation is a must in portfolio. Current drop in global gold and silver prices coupled with Rupee strength offers a good opportunity to enter in our view.

FX

We expect the Rupee to trade sideways in 93.40-95.80 over the next several weeks.