Billionz Multi-Asset Weekly Newsletter

Risk Sentiment Improves Amid Cooling Oil Prices

Global Developments:

Prospects of US and Iran reaching an agreement to extend ceasefire for 60 days during which there would be unrestricted passage through SoH and negotiations on Iran’s nuclear program lift sentiment. Energy prices cooled off, leading to a rally in bonds and equities. Dollar was weaker against most major and EM currencies this week. Trump is however yet to sign the agreement.

The WEF Chief Economists’ Outlook highlighted global growth concerns and indicated the possibility of a stagflation like scenario. However, most of the Economists surveyed expected India to be the brightest growth story over the next 12 months on infrastructure spending and domestic manufacturing and saw imported inflation as being the key risk

Key event to look forward to next week would be the US May jobs report and RBI policy on Friday.

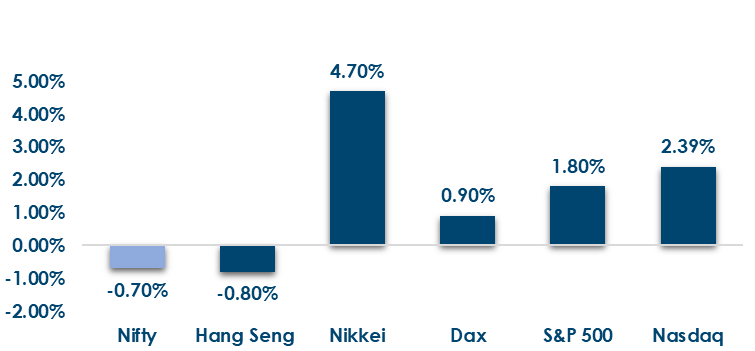

Global Equity Markets:

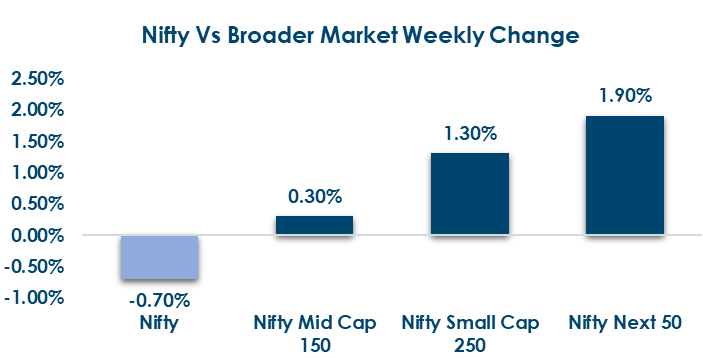

Domestic Equities:

- The Nifty 50 trades at 19.6x trailing and 18.7x forward earnings, reflecting relatively reasonable large-cap valuations.

- Midcaps (30.1x) and Smallcaps (24.2x forward) continue to command a significant premium, indicating elevated growth expectations.

- FPIs withdrew net USD 3.5bn from domestic equities in May, third successive month of FPI selling.

- India VIX ended at 16.18 compared to the previous week close of 17.91.

- Institutional flows remained supportive this week, with DII inflows of ₹25,803 crore more than offsetting FII outflows of ₹23,735 crore.

- Stock-specific action remained strong this week, with Wockhardt (+29%), Cemindia Projects (+24.2%) and Emmvee Photovoltaic (+23.1%) leading the gainers, while Techno Electric (-19.1%) and Poly Medicure (-15.6%) were among the top losers.

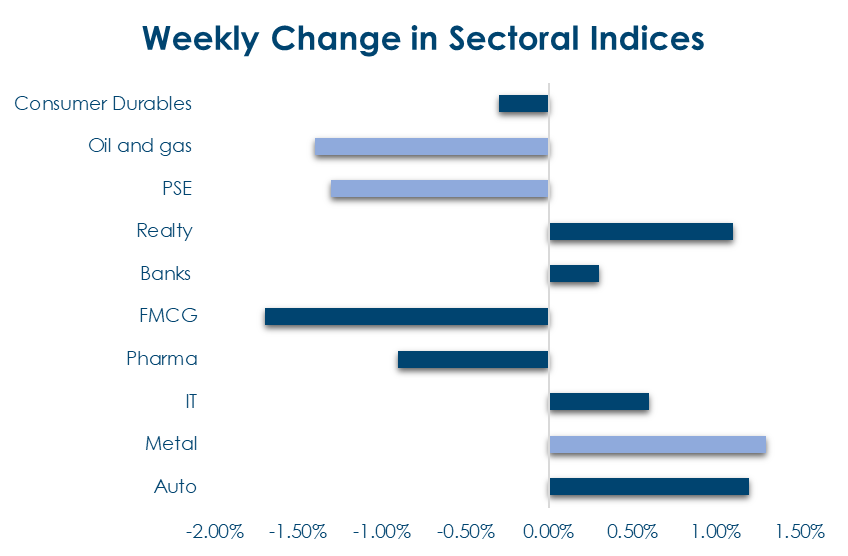

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income:

Global Rates:

Global bond yields declined across major economies this week, led by Switzerland (-16bps) and the US (-12bps), as easing energy prices and improving risk sentiment supported fixed-income markets.

India Rates & Flows:

Domestic rates softened, with the 10Y G-Sec yield easing 9bps to 7.00% and 1Y OIS falling 20bps to 6.08%, while FPIs invested a net USD 400mn into Indian debt during May.

Real Estate:

- SILA raised fresh capital from leading Indian family offices, underscoring strong investor interest in asset-light real estate service platforms.

- The funding will support technology upgrades and business expansion as SILA scales its presence across India’s growing commercial and industrial real estate markets.

IPOs:

- SME IPO activity picks up next week with Merritronix (₹70 crore) and Aureate Tradde (₹27 crore) collectively raising ~₹97 crore, while the mainboard market remains largely inactive.

- Merritronix offers exposure to defence and aerospace electronics manufacturing, while Aureate Tradde is positioned in the EV supply chain through its distribution of lithium-ion and sodium-ion battery cells.

Private Equity & Venture Capital

- PE/VC funding remained muted at ~$57 million across 21 deals, with investor interest focused on healthcare, consumer, technology, and real estate services.

- M&A activity was led by Anupam Rasayan’s acquisition of a 43% stake in Bliss GVS Pharma, strengthening its pharmaceutical footprint.

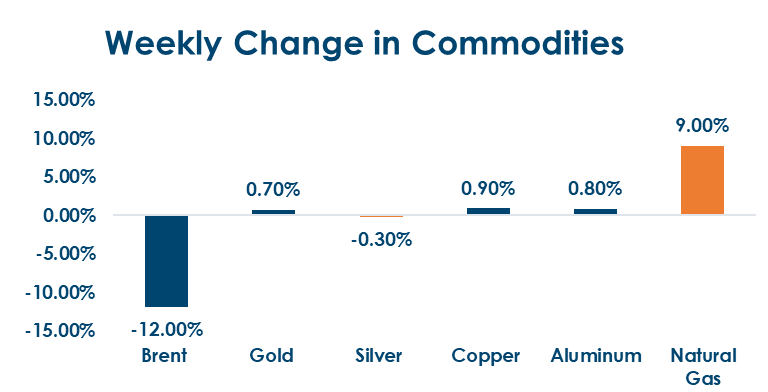

Commodities:

Commodities: Crude oil prices declined sharply this week, with Brent and WTI down 12% and 9.3% respectively, amid easing geopolitical concerns. Base metals remained firm, while gold edged higher and US natural gas outperformed with a 9% gain.

What’s New in the World of Wealth Management:

FPI equity outflows in CY2026 have crossed ₹2.1 lakh crore, the largest annual withdrawal on record, driven by geopolitical uncertainty, elevated crude prices, Dollar strength, and Rupee weakness. Foreign ownership in Indian equities has declined to a 14-year low of 14.7%, falling below domestic institutional ownership, while resilient DII and SIP inflows continue to provide stability to the market.

SEBI announced a series of measures to deepen India’s debt markets, including a DLT-based bond tokenization pilot, proposed bond ETFs, corporate bond index derivatives, and a simplified regulatory framework for debt issuers and intermediaries. The reforms aim to improve transparency, liquidity, and broader participation in the corporate bond ecosystem.

Our Views: What we Like?:

Equities:

Nifty50 underperformed global peers this week on a sharp, sudden sell off in late Friday trading. Gap support around 23100 is extremely crucial. Broader markets are outperforming the benchmark. As the index consolidates, it is time for active sector allocation and stock selection. We are overweight Financials and IT in our model portfolio.

Fixed Income:

RBI policy is due on Friday in coming week. We expect the RBI to hold rates to support growth given that Rupee has come off from lows. We expect the Yield on the domestic 10y to trade a 6.85-7.15% range over the next few weeks.

Commodities:

Crude will remain vulnerable to headline news. Overall we are bullish commodities, especially precious metals and base metals. We believe it is an opportune time to add Gold to portfolio given the correction in both USDINR and global Gold prices.

FX:

Rupee has strengthened 2% from lows but further room for appreciation is likely to be limited even if the geopolitical situation normalizes completely. RBI has a massive short position in forwards, which it would want to square off.