Billionz Multi-Asset Weekly Newsletter

Staying Invested Through Global Market Shifts

Global Developments:

Reopening of the Strait of Hormuz and passage of vessels through the Strait drove down energy prices and therefore inflation expectations and global bond yields.

De-crowding in Semicondictor names pushed US equities lower, stoking a contagion in Asian chip manufacturers as well, especially in Korea.

Dollar strengthened despite lower US yields as confidence in Fed’s commitment to reigning in inflation was restored after Kevin Warsh’ first policy. Stronger Dollar pushed the commodity complex lower in general.

Key data point to look forward to in coming week would be the US June labor data due on Friday.

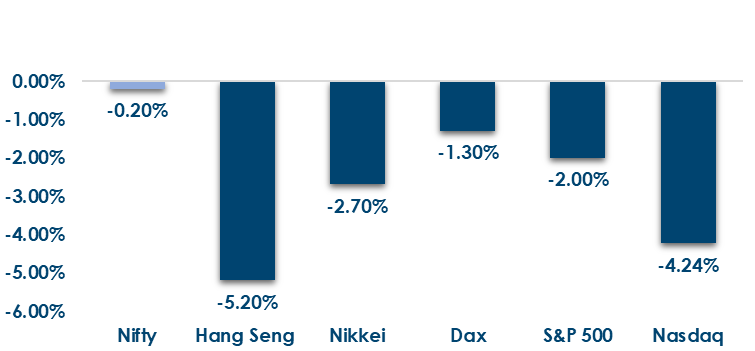

Global Equity Markets:

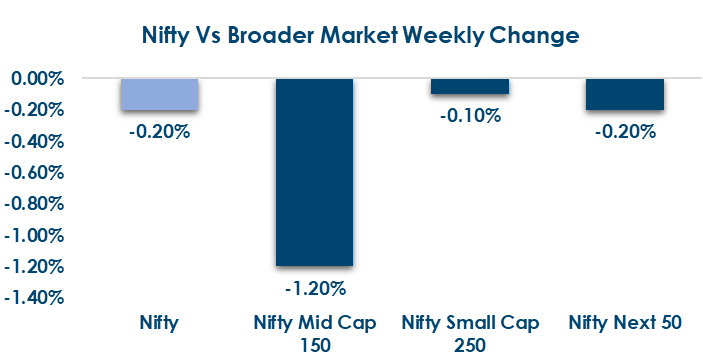

Domestic Equities:

- Nifty50 valuations remain relatively comfortable, trading at 20.8x trailing earnings and 18.5x forward earnings, reflecting stable earnings expectations and offering relatively better value compared to broader market segments

- Midcap and Smallcap valuations continue to remain elevated, with the Midcap100 at 29.7x/24.5x and the Smallcap250 at 27.3x/26.0x on trailing/forward P/E basis, suggesting that investors continue to price in strong growth expectations despite recent market consolidation.

- FPIs have sold net USD 5.5bn of domestic equities in June so far.

- Kirloskar Oil Engines, Oracle Financial Services, and Aegis Logistics were the top gainers this week, rising 24.8%, 13.9%, and 13.2%, respectively.

- National Aluminium, IFCI, and MMTC were the top losers, declining 11.7%, 10.2%, and 7.9%, respectively.

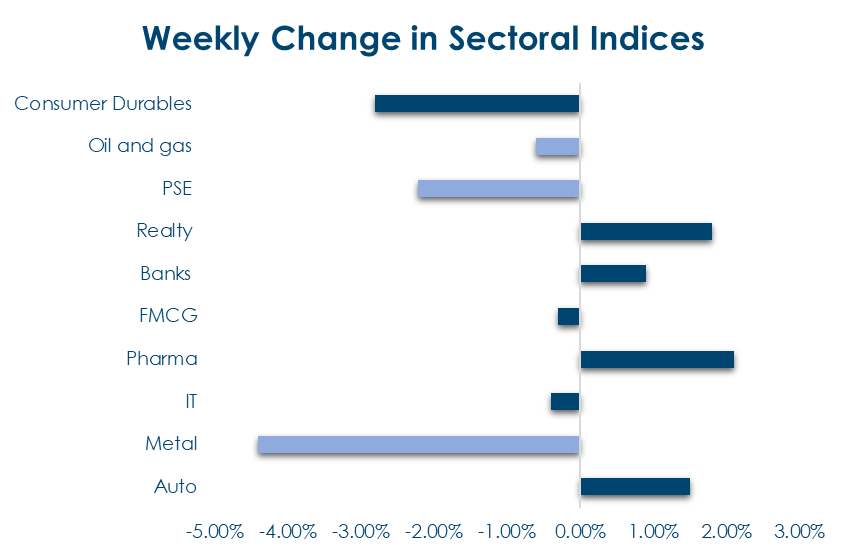

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income:

Global Rates:

- Global bond yields declined across major economies this week, led by the US 10-year Treasury yield, which fell 14bps to 4.37%, as easing energy prices and lower inflation expectations supported global fixed-income market

India Rates & Flows:

- In India, the 10-year benchmark yield softened by 8bps to 6.77%, while FPIs remained supportive, purchasing a net USD 5 billion of domestic debt in June so far, reflecting continued investor confidence in local fixed-income markets.

Real Estate:

- Rising demand, favourable demographics, and growing institutional interest are positioning senior living as a high-potential alternative real estate asset class.

- RMZ and Colt Data Centre Services are exploring expansion to up to 3GW capacity, reflecting strong investor confidence in India’s rapidly growing data centre sector.

IPOs:

- Seemax Resources’ ₹20 crore SME IPO will open on June 30 and close on July 2, with proceeds earmarked for capex expansion and debt reduction.

- While Ujin Pharma has filed its draft papers with SEBI, investor attention continues to centre on Jio Platforms, with SEBI seeking clarifications ahead of what could become India’s largest-ever IPO.

Private Equity & Venture Capital:

- Large-ticket deals continued to drive activity, led by Meta’s $900 million investment in Cred and SquareYards’ $95 million fundraise from EAAA Alternatives.

- Investor interest remained robust in AI, enterprise technology, sustainability and consumer businesses, with startups attracting backing from leading global and domestic investors.

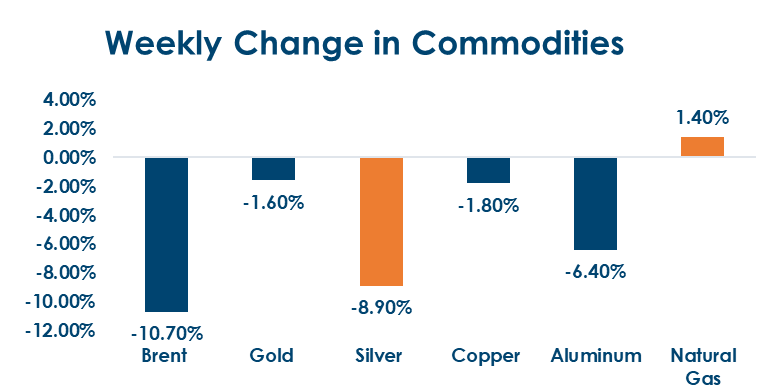

Commodities:

Commodity prices corrected sharply this week, led by a steep decline in crude oil and precious metals, as easing geopolitical tensions, a stronger US dollar, and lower inflation expectations weighed on the broader commodity complex.

What’s New in the World of Wealth Management:

The week’s biggest fundraise news is the IRFC OFS. The government announced plans to sell up to a 2% stake in IRFC via offer for sale, looking to raise around ₹4,200 crore to meet its disinvestment target for the year. On the QIP side, Equitas Small Finance Bank’s board approved raising ₹500 crore through NCDs and ₹1,250 crore through a QIP, while City Union Bank approved a QIP of up to ₹500 crore, subject to shareholder approval in August, to support its capital base and growth plans. Block deal activity was also active. Bain Capital fully exited Emcure Pharma after 12 years through a ₹352 crore block deal, alongside a separate ₹130 crore share sale by Global Health co-founder Sunil Sachdeva. On the regulatory front, SEBI is reportedly considering allowing celebrity endorsements for market entities, with safeguards to keep disclosures accurate and not misleading for retail investors.

Our Views: What we Like?

Equities: Nifty50 seems to be stuck in 23600-24300 range. Gap support around 23600 and a higher low around 23770 are extremely crucial supports. We do have a slight positive bias though.We believe we could see a protracted period of consolidation and therefore taking active sector and stock bets are crucial. We are bullish IT, Chemicals, REITs and Fin Nifty in our model portfolio.

Fixed Income: Worst seems to be over for bonds and rates as well. We expect the 10y yield to remain in 6.70-7% range over the next several weeks. Extending duration and deploying a carry roll down strategy can be considered given rich term premium.

Commodities: We do not believe we have a breakout on Dollar index as of now and prefer to wait for confirmation.As a result we stick to our long precious metals and base metals view. Crude is almost down to pre-war levels and we see limited downside from current levels.

FX: We expect the Rupee to remain range bound as well in 93.40-96.40 over the next several weeks.