Billionz Multi-Asset Weekly Newsletter

Fragile US-Iran Ceasefire Drives Market Volatility

Global Developments:

Strikes from both sides i.e. US and Iran followed by comments from Trump that ceasefire with Iran was over, jolted risk sentiment.

Immediate ask from US is that Iran declare the SoH open to shipping and assure that they will not attack transiting civilian vessels

This caused crude prices to spike again, bond yields to rise, equities to correct. FX continues to be in its own low volatility regime.

There is an ebb and flow to the sentiment around AI as well with some sections of the markets worried about the fact that there has been over investment in that space.

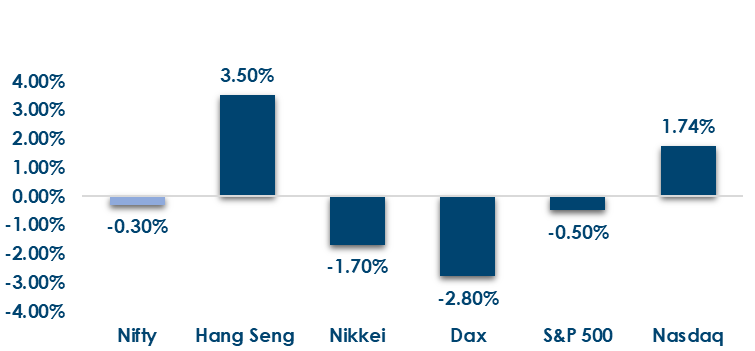

Global Equity Markets:

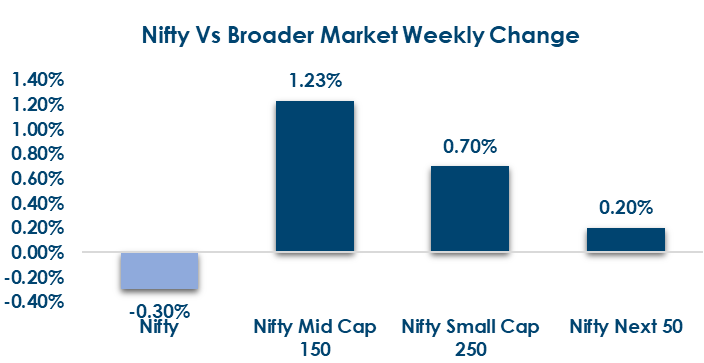

Domestic Equities:

- Nifty50 trades at 20.2x trailing PE and 19.2x forward PE, indicating relatively reasonable large-cap valuations.

- Midcap100 trades at 30.4x/31.3x, while Smallcap250 trades at 28.0x/26.4x (trailing/forward PE), reflecting richer valuations in the broader market.

- FPIs have invested net USD 1.6bn in domestic equities in July so far.

- Jewellery and financial stocks outperformed, led by Kalyan Jewellers (+24.6%).

- Trent declined 13.1%, while JSW Dulux (-10.5%) and Dr. Reddy’s (-9.5%) also ended the week lower.

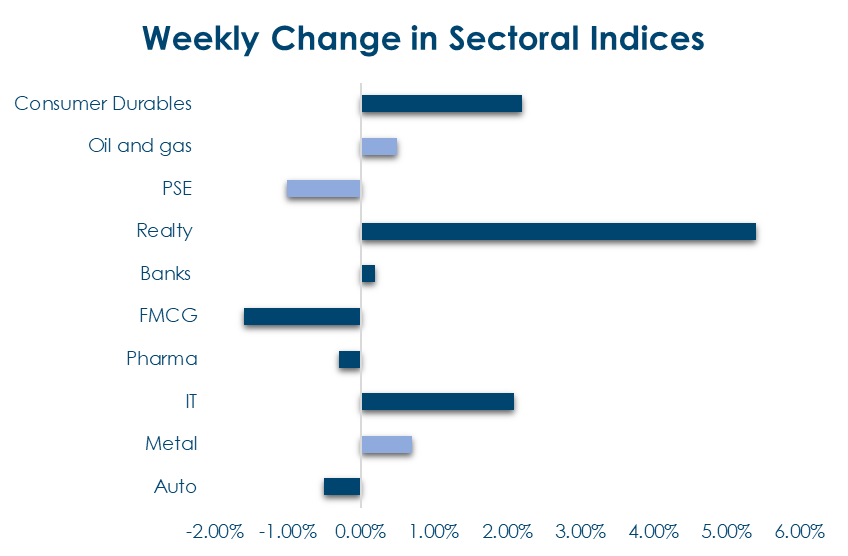

Below are the graphical representations for how key benchmark indices performed this week& how sectoral indices performed this week:

Fixed Income

Global Rates:

- Global bond yields moved higher this week, led by Germany (+12bps) and the US (+9bps), reflecting firmer rate expectations, while Japan’s 10Y yield declined 9bps.

India Rates & Flows:

- India’s 10Y G-Sec remained stable at 6.71%, with ample banking liquidity (~₹1 lakh crore surplus) and USD 1 billion of net FPI inflows into domestic bonds so far in July

Real Estate:

- Institutional interest remained strong as Arnya RealEstates Fund invested ₹100 crore in a Mumbai residential project, while hospitality-focused land acquisitions continued to gain traction.

- Blackstone-backed Ventive Hospitality agreed to acquire Kelzai Eco Reserves, which owns a 420-acre property, highlighting ongoing interest in strategic land banking and hospitality-linked real estate opportunities.

IPOs

- The primary market enters a busy week led by the ₹11,693 crore SBI Funds Management IPO, the largest mainboard issue in recent months and a key gauge of institutional investor sentiment.

- Alongside Alpine Texworld and Millworks Technologies IPOs, four companies are set to list, highlighting strong momentum in India’s primary market activity.

Private Equity & Venture Capital

- Private equity and venture capital funding moderated for a second straight week, with 21 companies raising $121 million, as investors remained selective despite healthy deal activity.

- The week’s highlights included TPG’s acquisition of Aseem Infrastructure Finance (around ₹5,000 crore) and continued investments in healthcare, industrials, and education, reflecting sustained interest in high-quality growth businesses.

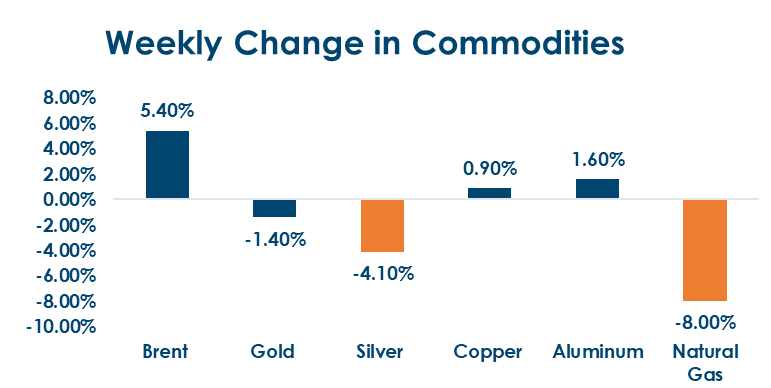

Commodities

Commodity markets witnessed mixed performance this week, with energy prices rallying on renewed geopolitical tensions, while precious metals retreated amid easing safe-haven demand.

What’s New in the World of Wealth Management

The week’s most significant structural development came from SEBI, which approved the launch of futures and options on the Nifty India FPI 150 Index, a gauge of 150 stocks selected based on their accessibility to foreign investors, the kind of metric that global benchmark providers like MSCI typically use to decide index membership. This is a meaningful market structure move: onshore derivatives on an FPI-friendly index give global institutional investors a new hedging tool and could strengthen India’s case for broader index inclusion over time. DIIs were net buyers of Rs 2,057 crore in the cash segment on July 10, continuing their role as the market’s primary support layer. On the primary market side, Kusumgar Ltd’s IPO entered Day 2 of subscription on July 10, looking to raise Rs 650 crore entirely through an OFS, with a price band of Rs 398 to 419 per share and listing on BSE and NSE scheduled for July 15.

Equities

Our bias is to the upside barring any massive negative external shock. PI flows picture seems to be turning around. While near term range for the Nifty50 is 23600-24600, break above 24600 could cause a brisk 5% rally.

Fixed Income

US 10y yield is at crucial levels around 4.60%. Real yields in US are quite elevated. India benchmark 10y bond yield is expected to be in 6.60-6.90% range over foreseeable future. We believe 5y OIS is a receive on upticks. 5y MIFOR is also a receive in our view.

Commodities

We expect US real yields to cool off and therefore are bullish commodities. We expect Gold and Silver to be supported around current levels and believe its a good investment opportunity from a 3-5y investment horizon perspective.

FX

We see the Rupee remain range bound in 94.90-95.80 in the coming week and expect it to trade a 93.40-97 range over the next several weeks.